Updated Every Two Weeks

This week, we saw a major dispute unfold between Zambia and private sector lenders, who rejected the government’s request for a 6 month payment holiday, due to Zambia’s needs to spend on COVID19 management. The private sector lenders rejected this request, and by doing so fuelled concerns that “Africa” would be falling into a debt crisis due to COVID19.

This kind of action and speculation is unfortunately, as we recognised when we began to collate the data on COVID19’s impact on Africa, highly problematic. Not only does it label Africa’s 55 countries as one, it also appears to be based on information that is contrary to the data in the public eye and cannot be rationally explained.

Take our findings this week.

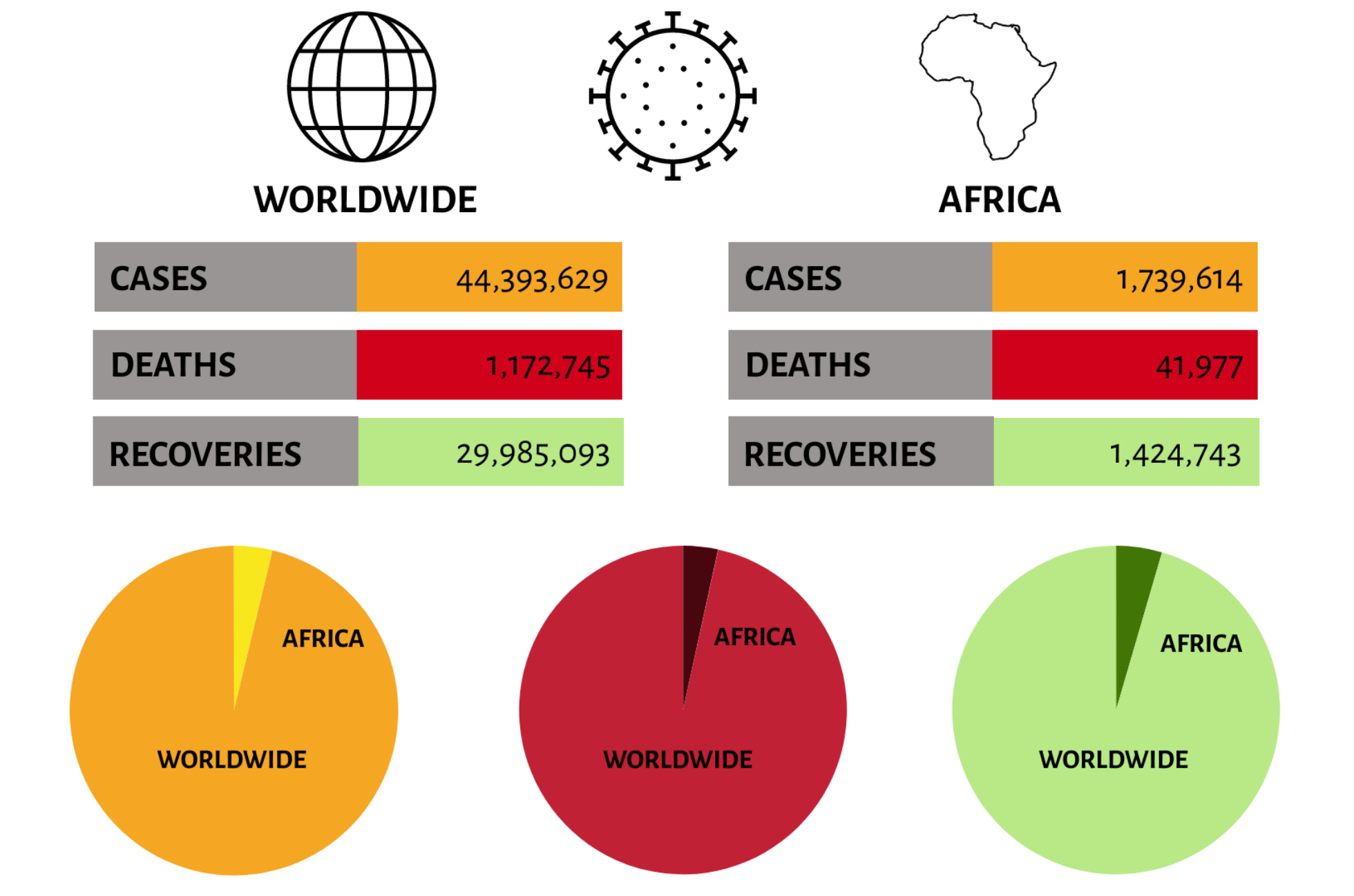

This week, we see that there is still no “mass outbreak” across the continent – meaning Africa as a whole has considerably less cases than the rest of the world. However, cases continue to fluctuate in different countries, with some countries worried about “second waves”, others simply still doing their best to manage a slowly rising trend, and yet others seeing low case numbers and over 95% recovery rates. We can expect the same much into 2021.

This varied experience also applies to the issue of debt. As we have shown in previous infographics – Africa as a whole has a very small proportion of debt from other governments, multinational banks or the private sector globally – $775 billion in total, comparable to amounts held by single countries (e.g. Brazil’s $557bn, or India’s $521bn) and less than half of what China has borrowed from the world ($1962bn).

However, over the next four years, as forecast by the IMF, debt in many countries is expected to fluctuate in some African countries. For instance, some 5 countries are currently forecast to see a “second wave” of debt to GDP ratios above those they saw in the early 1990s when a previous “African debt crisis” was declared. However, these 5 countries don’t include Zambia – they are Cabo Verde, Mauritius, Mozambique, South Africa, and Tunisia… countries that are often “seen” to be well managed. Other countries are simply doing their best to manage the steadily rising costs of COVID19 health and economic costs, and yet others are seeing hardly any changes because they have so little access to international sources for loans.

So why are there fears of an “African Debt crisis”?

Well, with the IMF projecting slower 2021 growth rates globally – as we shared in our last infographic – it is right to be worried about economic management by governments all over the world. But just as the world got African management of COVID19 wrong, it is possible the world is getting African economic management wrong too. Take Zambia. Up to 2025, Zambia’s debt levels are forecast to reach 120% of GDP. That might seem high, but at the height of the 1990s Zambia had debt of up to 261% of GDP. With over 17,000 COVID19 cases detected so far, 94% of whom are recovered, and over 310,000 tests completed, the challenge for Zambia is reigniting growth which is predicted to only reach 0.6% in 2021, and 1.2% thereafter. How to do this without borrowing?

The fact is, most African governments are working hard to increase economic growth and grow resilience in the time of COVID19. It’s time the world didn’t succumb to old, tired “one-story” narratives, and made more cheap finance available to enable African citizens to truly recover.

*** The End***

To find out how Development Reimagined can help you, your organisation or Government during the COVID-19 outbreak please email the team at clients@developmentreimagined.com .

Special thanks go to Rosie Wigmore, Rosie Flowers, Sophia Kladaki, Rosie Flowers and Jing Cai for their work on the graphic and collecting/analysing the underlying data.

The data was collated from a range of sources including: government websites and media reports, the IMF policy tracker; the US Chamber COVID19 Dashboard; Our World in Data, Africa CDC and Worldometer. Our methodology is entirely in-house, based on analysis of spending, social distancing, income categories and other trends.

If you spot any gaps or have any enquiries, please send your feedback to us at DRteam@developmentreimagined.com, we will aim to respond asap.

November 2020