IMF released a new Africa-focused report

In a recent address to the 3rd Pan-African Parliament Summit, the President of Kenya William Ruto remarked: “The discursive profile of the continent has too often been focused on the challenges and difficulties we face and the assistance we need, in a way that depicts us as chronically subordinate, eternally vulnerable.”

He was right. In April, the IMF released a new Africa-focused report, which looks at the continent’s economic growth outlook for the years ahead. The report argued that ongoing global challenges and economic shocks from climate, to the Russia-Ukraine War, will impact the continent the most. It was not surprising. “Alarmist” reports, which brush over the continent are widespread, and portray African countries as passive actors unable respond to crises.

However, in contrast, African countries COVID-19 resilience is one example of how proactive policy measures by African leaders mitigated the spread of the virus. Further, really examining the data, there were three other key takeaways to keep in mind from the report that were overlooked.

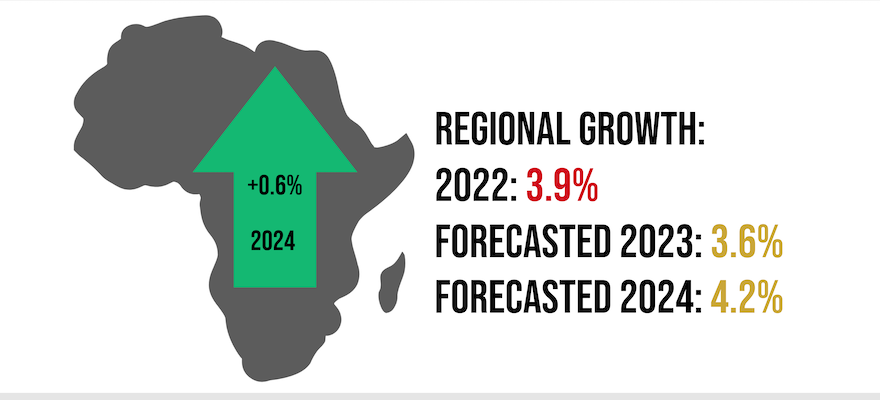

First, aside from 2021, the IMF’s outlook for Africa as a region has been ahead of global forecasts. However, African regional growth slows down for two consecutive years – 3.9% and 3.6% in 2022 and 2023, respectively, due to a “big funding squeeze” from limited aid and access to private finance. Nonetheless, 39 African countries are still forecast to demonstrate faster economic growth than the total world growth in 2023. Moreover, regional economic growth is projected to rebound by 0.6% to 4.2% in 2024 when a global recovery sets in with reductions in inflation and monetary policy tightening. Whilst the rest of the world has a gloomy outlook, African countries will spearhead global economic growth.

Second, although African countries account for over 50% of countries within the top 10 fastest-growing economies globally in 2023 and 2024, the World Bank and IMF’s Debt Sustainability Analysis (DSA) singles out African economies. For instance, in 2024, six out of the seven fastest-growing African economies are classified as in moderate or in “debt distress” – the exception being Libya. This is of course not limited to African countries experiencing high-growth – as over half of the 70 countries on the IMF and World Bank’s DSA list are African. African countries account for almost all “in debt distress” ratings, aside from one non-African country – Grenada. As such, African countries will be continually constrained by the DSA despite having high forecasted economic growth, showing there is clearly an inherent bias in the DSA system.

Third, it is higher borrowing costs from monetary policy tightening elsewhere that is constraining Africa, not internal growth dynamics. Although the IMF has disbursed some emergency funds to support countries to manage and recover from the COVID-19 pandemic, they have not been at the scale required, and many have been short-term and relatively expensive. Indeed, the constrained fiscal space for African countries generated by higher interest rates risks constraining potential future growth, especially when there are huge infrastructure financing gaps which need to be closed through external financing. Our latest analysis shows that for four African countries which are classed as either in “high debt or in debt distress” have annual infrastructure investment needs which range from US$7 billion to US$34.8 billion to meet the Sustainable Development Goals (SDGs).

So why does all this matter? Well narratives hold power, even if the data doesn’t actually support them. And, publicising narratives – with economic tools – that leave out the role of growth on the continent reinforces white saviour complexes, with “simple fixes”. This results in the IMF and others placing emphasis on reform of borrowing countries – rather than the need to reform the international financial system as a whole.

The reality is we are in a complex world, where there are no simple fixes. There is a need for real, feasible action which needs to be taken into account by the IMFs shareholders, not just its borrowers. The most recent IMF report attempts this by going beyond the typical “US-China competition” dynamic, but there is a need for more specific, holistic solutions – such as regulation of credit rating agencies or regulation of external interest rate rises, or of reform of its own instruments like DSA, that the IMF could call for, and would really make a difference. Without these major shifts, the IMF will remain still stuck in the past.

The upshot? Two things. First, growth on the African continent is rebounding. Second, the IMF needs reform if it is to really service African countries in the way they need.

To find out how Development Reimagined can support you, your organisation or Government to review key economic response policies to the COVID19 crisis, the Russia/Ukraine war and other shocks please email the team at clients@developmentreimagined.com.

Special thanks go to Christy Un, Rugare Mukanganga, Kofi Owusu-Koranteng and Jade Scarfe for their work on the graphics, collecting/analysing the underlying data and sharing this accompanying article.

The data was collated from a range of sources including: government websites and media reports, IMF and World Bank data and Statista. Our methodology is entirely in-house, based on analysis of economic growth, inflation and other trends.

May 2023