Updated Weekly

Last week, our regular infographic update highlighted the actions and challenges African countries are facing in directly managing the COVID19 health crisis.

This week, prompted by a concern that economic woes on the continent appear to be being blamed on “lockdowns” we wanted to check the facts on behalf of our clients, analysts and investors, and explore the potential effects on Africa of the global economic slowdown (i.e. due to COVID19 challenges elsewhere). Our analysis reveals that we need to take the effects of global slowdown seriously, and as usual there is a mixed picture. There are some African countries that are forecast to be more resilient to the slowdown and others that will have major recovery challenges – but not necessarily the usual suspects on both sides.

So which African countries will be most resilient to the COVID19 global slowdown?

While we typically look at countries in much more bespoke detail for our clients, we do also draw on the broader economic models and forecasts out there, such as those from the IMF. Interestingly, while the headline when the latest IMF forecasts came out in April 2020 was “the worst reading on record” for Africa, our analysis reveals that 23 African countries are expected to have positive (above zero) growth in 2020, despite COVID19. This includes countries that were previously on the IMF’s “top 10” list for global growth in 2020, such as Rwanda, Ethiopia, Senegal, Cote D’Ivoire, as well as Benin, Guinea, Uganda and South Sudan, which is one of the poorest countries in the world but still forecast to grow faster than all other economies globally in the COVID19-inflicted 2020, primarily due to oil demand from China.

In addition, if we look at “resilience” – as in are some countries predicted to be able to weather the COVID19 storm better than others – we find that the majority of African countries perform somewhat better than the rest of the world. The IMF predicts that only 13 African countries will face an over 6.3 percentage point drop (the average percentage point drop for the world and Africa due to COVID19)…. including Libya whose economy is forecast to contract by over 50% in 2020, in particular due to conflict.

So which African countries will be most vulnerable to the COVID19 global slowdown?

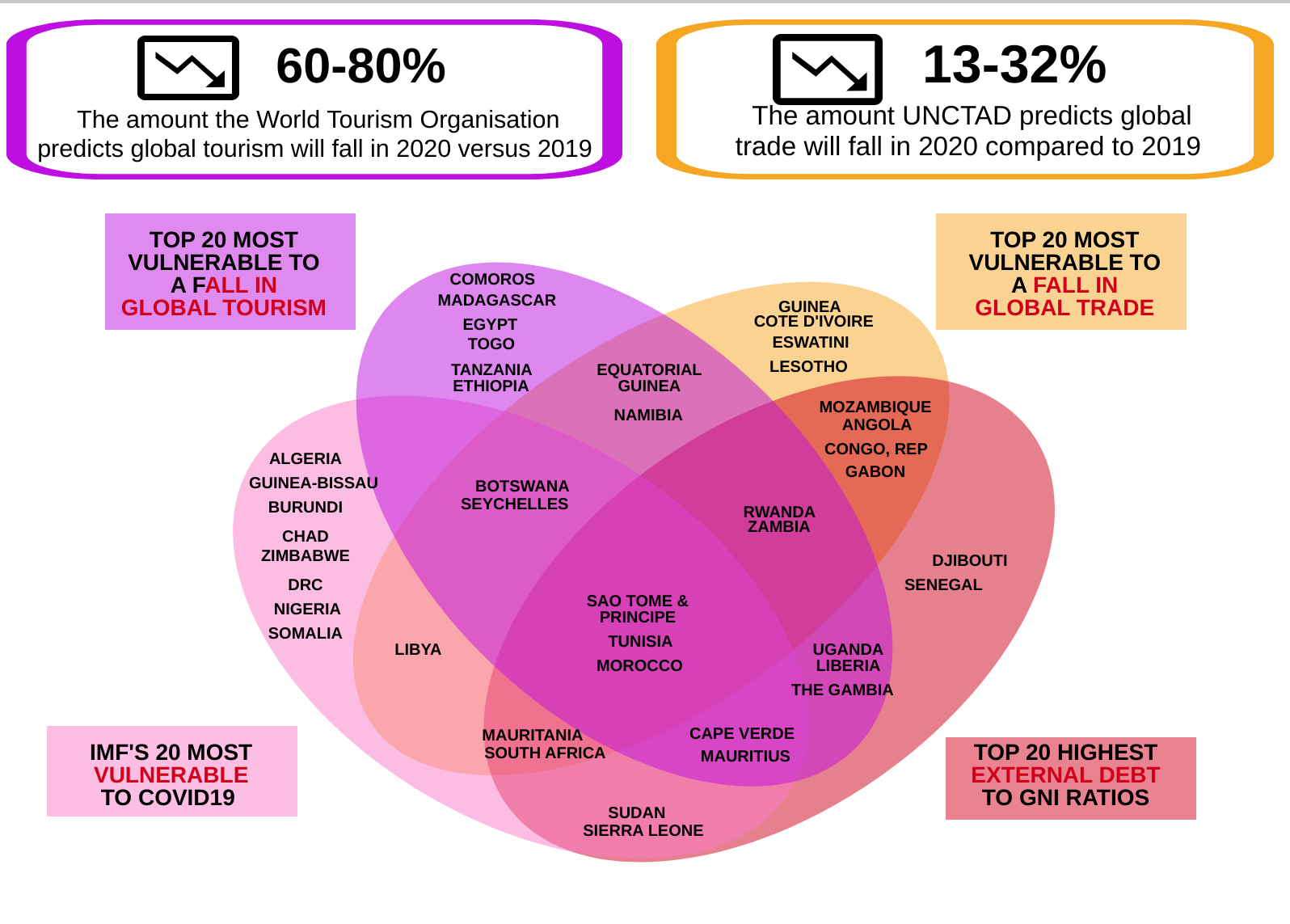

The challenge with forecasts like the IMF’s is that while useful, they hide a great deal of specificity. Although Africa accounts for less than 4% of global investment, tourism and trade, the fact is there are many African economies that depend on all of these “flows” hugely for growth. And most of these “flows”, according to various UN and international organisations, are due to drop massively in 2020 – whether or not African economies themselves lock down.

Our analysis this week explores this, by first identifying the most vulnerable 20 countries across the continent in both exposure to trade and tourism, and overlaying this with the IMF’s analysis (in terms of percentage point drops) as well as figures of countries’ indebtedness. The results may surprise those that do not follow African economies in depth as well do. While some of Africa’s largest economies such as Nigeria, South Africa and Egypt do appear on our “vulnerability matrix” or “Venn diagram”, many others which are seen as very “stable” (such as Rwanda, Senegal and Ethiopia) also appear, and some economies that have been subject to “downgrading” by traditional ratings agencies in particular for external debt issues do not appear at all (e.g. Kenya).

Our analysis highlights the countries that will face major challenges, which we know are already being felt by countries such as Mauritius and Seychelles who appear on the matrix yet are – like New Zealand – already in a “post-COVID19” environment. Our analysis also raises some major questions about how country risks are being assessed with regards to COVID19 by ratings agencies and others, an area that we plan to investigate further with partners in due course.

So, what are countries doing to counter these challenges?

First, African countries are continuing to roll out new measures and expand their budgets for COVID19 response. The number of pro-poor measures we have tallied is now 220 (a rise of 23 from two weeks ago), and the budget has risen by $4bn over the past two weeks, which translates to an average 2.5% of GDP (current) being spent by African countries. That’s a big uplift, both across middle-income and low-income countries. Togo and Lesotho in particular stand out as making significant efforts. We have also detected a trend in many new measures being targeted towards the Agriculture sector, to especially to deal with food security concerns. That said, some countries such as Somalia, Angola and Algeria seem to be very behind others in both budget and economic policy terms.

Is the international community rallying around to help?

Development partners are continuing to expand their support for African countries with new loans and grants. The data we have collated shows that direct pledges from development partners adds up to just over half of this spending, excluding debt relief measures and medical teams/equipment-based aid. This is a rise from around a third two weeks ago, and it is clear that this additional finance could fill some major gaps.

However, loans from the IMF make up over 80 percent of this finance from the intentional community (as opposed to grants), and of those loans, 65% have gone to some of Africa’s largest economies – leaving very little wriggle room for smaller African nations to manage the economic fallout from global slowdown.

With this new analysis in mind – we can only reiterate our three recommendations from two weeks ago.

To African governments – Keep going. Continue to ramp up the economic and poverty support measures, coordinate requests for support to get the best results, and learn from each other.

To private sector actors and development finance institutions – do not just take headline numbers for granted. Look in depth at each country and look at investing in Africa more now rather than turning the taps off.

And finally, to Africa’s development partners. Keep going, especially in providing grants to the most vulnerable low-income countries identified in this analysis. The more African countries that can weather the storm the better for the world.

Digest our data below.

To find out how Development Reimagined can help you, your organisation or Government during the COVID-19 outbreak please email the team at clients@developmentreimagined.com .

Special thanks go to Rosie Wigmore, Rosie Flowers, Angela Benefo, Chazha Macheng and Wang Yu for their work on the graphic and collecting/analysing the underlying data.

The spending/policy measures data was collated from a range of sources including: the Milken Institute Africa Tracker; the IMF policy tracker; the US Chamber COVID19 Dashboard; a tracker of social support measures by Ugo Gentilini, as well as government websites and media reports. Other COVID19 data was collated from our world in data and Africa CDC. Data for most vulnerable countries was collected from the IMF’s October 2019 and April 2020 World Economic Outlooks, and World Bank sources including the International Debt Statistics database, and the WITs database. Our methodology for classification is entirely in-house, based on analysis within four social measures categories and spending data gathered.

Note that for spending data, we have excluded “non-specific” and “non-financial” contributions to Africa such as finance for the Africa CDC, the Jack Ma Foundations donations of medical equipment, or Chinese government medical teams (see our analysis from last week here).

If you spot any gaps, please send your feedback to us at drteam@developmentreimagined.com, we will aim to verify and rectify asap.

May 2020